The role of cash in SIPPs with Insignis Pension Director, Sarah Smith

This article is intended for financial services professionals only. None of the information contained in this article should be received as advice. Pensions are a complicated area of financial planning and IPM suggests that financial advice from a suitably regulated financial adviser is sought before an individual takes any action in respect of their pension savings.

The latest figures from the FCA suggest that there are over 6 million SIPPs in the UK as of November 2025, with benefits valued in excess of £650 billion.

Of this amount, over £120 billion is held in bespoke SIPPs, such as IPM’s, for over 300,000 individuals. In our own adviser survey in late 2024, 82% of all advisers we asked said that they are either recommending the same number or more of bespoke SIPPs than they were three years previously.

We recently considered the SIPP market being split into three different types of SIPPs: online, simple, and bespoke. While many clients’ needs can be met by an online or simple SIPP solution, our research suggests that there is a continued and growing demand for a “full” SIPP, offering a variety of investment options.

We also put together five of the different scenarios where a bespoke SIPP may help your clients, which you may find helpful.

Regardless of which type of SIPP you select, they will all have one thing in common: the ability to hold cash.

Breaking down how SIPPs hold cash

A SIPP like IPM’s will have a trustee bank account that all monies in and out of the SIPP must pass through for reconciliation purposes. Each provider will have their own terms upon which this account must operate; some will require a minimum balance to be held, for example. The level of interest will also vary depending on your chosen provider.

IPM’s trustee bank accounts are operated by Metro Bank. The rate of interest payable is displayed on our website at all times; we do not require a minimum balance to be held in this account (unless we are paying regular income drawdown or mortgage payments) and IPM does not apply a fee to make alternative investments within the SIPP, including cash investments.

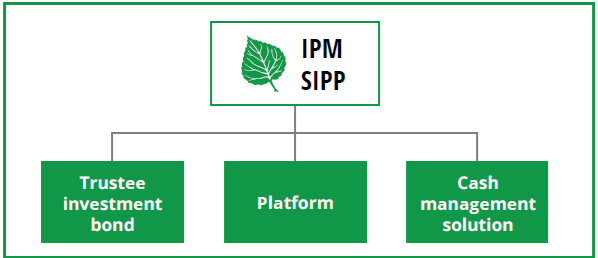

Where people elect to hold cash as part of an investment strategy, we have seen this applied in a variety of ways over the years. For example, they may:

- Choose to continue holding cash in the trustee bank account

- Hold cash with whatever options they have with their chosen investment house

- Open accounts with third-party banks that can hold deposits for SIPPs on an immediate access, fixed-term, or notice period basis

- Open a cash management solution; a platform for cash that gives clients and advisers access to a variety of different banks and accounts

- Hold certain types of NS&I products.

Any one of these options can be held alongside other investments in the IPM SIPP.

The role of cash has been brought more into focus in recent years, with the increases seen in the Bank of England base rate since late 2021 reflected in an increase in interest rates being offered in return for deposits.

Coming back to SIPPs, with pensions coming into the scope of IHT from April 2027, the role of cash could come into even more focus. This could be because there is a need to keep liquid funds to meet an IHT liability, or because people are considering an alternative approach to their pension withdrawal strategies.

In the four weeks leading up to the end of the 2025/26 tax year, the number of clients that drew benefits from their SIPP, either as a pension commencement lump sum or taxable income under flexi-access drawdown or UFPLS, was up 9% from the same period in 2024/25.

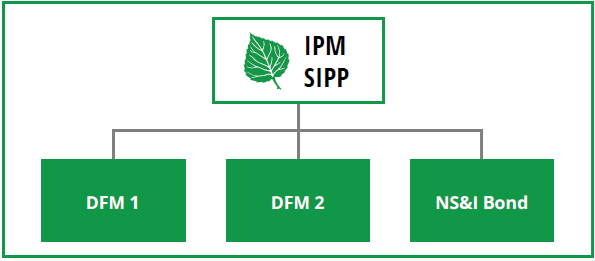

Certain NS&I products can be held by SIPPs. When the rates offered are attractive, these prove popular to our clients who are looking for a secure home for high cash values.

Over recent years, we have seen a reduction in the number of banks offering deposits directly to providers like IPM. In turn, several cash management solutions have come to the market, allowing advisers and clients access to place deposits with a variety of banks via an online platform.

IPM can work with any cash management solution subject to our own internal assessments being completed.

Insights into cash management solutions for SIPPs from Sarah Smith, Pension Director at Insignis

One such firm that provides a cash management option is Insignis Cash Solutions. Given the interest we see in holding cash in SIPPs, we asked their Pension Director, Sarah Smith, to give her opinion on the role of cash in SIPPs at the moment.

“Since 1 December 2025, the Financial Services Compensation Scheme (FSCS) deposit protection limit has increased following a review by the Prudential Regulation Authority. The change restores the real value of deposit protection, which had been eroded by inflation since the limit was last set in 2017.

“Under the updated rules, eligible deposits held with UK‑authorised banks, building societies, and credit unions are protected up to £120,000 per individual and £240,000 for joint accounts, per authorised institution. This replaces the previous £85,000 limit.

“The Temporary High Balance limit has also increased to £1.4 million per person, per institution for qualifying life events, including property sales, inheritance, and redundancy payments.

“While cash is often held outside investment portfolios to manage short‑term volatility or meet known liabilities, it is not risk‑free. Inflation can erode real value over time, and counterparty risk remains relevant should a deposit‑taking institution fail.

“FSCS protection applies per person and per authorised institution, not per account. Multiple accounts held within the same banking group are aggregated when assessing eligibility, including personal accounts, Cash ISAs, and pension cash.

“Using a cash platform can help address these limitations by providing access to multiple UK‑regulated institutions through a single point of administration. This allows savers to diversify deposits more effectively, maximise FSCS eligibility, and seek more competitive interest rates, while maintaining a consolidated view of their cash holdings.

Chart shows average deposit for client hubs available via the cash platform.

“As client hub types fall under the same FSCS eligibility limits per person and per institution, a central platform that spans multiple hubs and institutions offers an effective solution for clients seeking diversification and improved returns without the risk of over‑concentration.

“For pension savers, cash hubs help advisers maximise FSCS protection eligibility for pension-held cash, supporting risk management and liquidity planning during periods of market uncertainty.”

Insignis is not a deposit‑taker and does not provide FSCS protection directly; eligibility depends on the underlying bank or building society.

Get in touch

Email info@ipm-pensions.co.uk or call 01438 747151.