Revealed: Our tips to help you compare SIPP provider charges

This article is intended for financial services professionals only. None of the information contained in this article should be received as advice. Pensions are a complicated area of financial planning and IPM suggests that financial advice from a suitably regulated financial adviser is sought before an individual takes any action in respect of their pension savings.

One thing we regularly hear from advisers when discussing SIPP provider fee structures is that these can often be complex, particularly with bespoke SIPPs like IPM’s. This can make it difficult to ascertain exactly how much a client is likely to pay for their SIPP year-on-year.

We regularly review the charging structures of other SIPP providers and there are occasions for us too where we are not quite sure what a client would likely pay!

A big help, for both clients and advisers, was the introduction of Consumer Duty in July 2023. Part of the requirements for regulated providers like IPM was to produce Fair Value Assessments and Target Market Statements for their products. You can find these and all IPM’s Consumer Duty information on our website.

Simple, transparent fees

We recently looked at what we believe are the three different types of SIPPs there are in the market. IPM believes that our SIPP sits firmly in the full, bespoke SIPP category.

Those advisers familiar with IPM will know that we charge a flat annual administration fee of £580 plus VAT, regardless of the value of the fund. We increased this from £540 plus VAT in 2024; prior to this we had not increased our annual fee in over 23 years!

Our approach to fees is to keep them simple and transparent. IPM does not charge additional fees for:

- Accepting contributions

- Transfers into a SIPP*

- Making standard, UK-based investments

- Holding different standard investments within the SIPP

- Moving money to or from the trustee bank account, or for responding to emails or telephone calls.

*Additional fees can apply for some in-specie transfers

For those clients in drawdown, our annual drawdown fee of £150 plus VAT and a benefit crystallisation event fee of £150 plus VAT apply.

We also have one of the most cost-competitive offerings in the market for holding commercial property in SIPPs.

Why we believe scenario-based charging helps you to explain SIPP fees

Given the complexity of some charging structures of SIPP providers, we believe the easiest way to compare costs is to consider your client’s scenario and then apply the fees accordingly.

This is an effective way of comparing providers, as you can apply the charging structures of the providers of your choice to a specific scenario, thus giving you a side-by-side comparison.

You can then extrapolate these fees over the next 10 years to get an idea of the total cost to the client during this period.

Below, you’ll find some examples of how other providers’ charges compare to IPM.

Please note that the indicative costs for the other SIPP providers below are based on a random selection of full, bespoke SIPPs and do not accurately reflect any specific SIPP provider. Charges displayed are indicative of the charges displayed by full SIPP providers on their websites as of April 2026. The tables are for illustrative purposes only and should not be used for actual comparisons.

We have not considered online SIPPs or simple SIPPs for this comparison due to the fact that there are so many variables to each of these types of offering. For example, some may accept an asset class under a simple SIPP, but another may not.

The idea of sharing these scenarios is to show you the benefits of a simple fee structure and how scenario-based cost comparisons are an accurate and simple way of understanding a provider’s charges – especially compared with some of the complexities of our competitors.

These examples also show you why the way we charge is more straightforward for you and your clients and makes it easier for you to compare the relative costs of our SIPPs versus other providers. Note that VAT has not been applied to these charges.

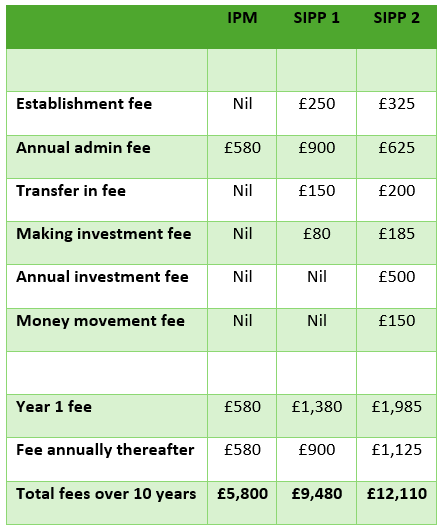

Scenario 1

In this simple and common scenario, your client wishes to:

- Set up a SIPP

- Conduct two cash transfers in

- Invest using a DFM

- Benefit from a platform

- Open a third-party bank account / cash management solution

When looking at full, bespoke SIPP providers, even a scenario that we see as common can produce a varying degree of fees.

Many SIPP providers will charge a fee to set up a SIPP. Often, clients will incur fees for holding more than one investment, or an investment that is deemed off panel. These can be charged either initially and/or on an ongoing basis. Care also needs to be given to “transaction fees”, i.e. where money is moving to / from the trustee bank account. For example, what is the impact on fees if your client is making a monthly contribution to their SIPP which is to be invested?

Scenario 2

In this scenario, your client wishes to:

- Set up a SIPP

- Conduct one “transfer in”

- Benefit from platform and trustee investment bonds

- Take the maximum PCLS and then pay monthly income.

Most providers will levy a fee for paying a PCLS and then an annual drawdown fee thereafter. What is more difficult to demonstrate, however, are the different charges that relate to how income is drawn.

Some providers charge more for higher frequency withdrawals, while some make an additional charge for ad hoc income payments. Note also the differing charges for investments.

Again, our structure means your client simply pays the same fixed fee every year, plus a one-off BCE fee. We do not charge to vary income amounts or payment frequency, or if the client wants a one-off payment.

In the above example, we also attempt to highlight that simply having two different investments in the SIPP can have a big impact on the fees you pay to some providers.

Scenario 3

In this third scenario, your client wishes to:

- Set up a SIPP

- Conduct one “transfer in”

- Make one contribution

- Purchase commercial property with borrowing

- Benefit from a platform account in the SIPP.

When we start looking at costs for commercial property purchase within SIPPs, this is where the cost benefits of the IPM SIPP really start to show.

IPM are well-priced for commercial property within a SIPP, mainly because we do not charge an annual property fee or annual borrowing fee on top of our annual administration fee. Most other providers will make this charge, and this is where the fees over a 10-year period can start to accumulate.

That said, cost comparisons for SIPP providers on property purchases are tricky. Many providers will charge a minimum fee or levy a time-costs charge.

The varying nature of holding a property within a SIPP will also make a comparison difficult. For example, IPM will charge a fee of £200 to put a new lease in place – but how regularly this fee will apply will depend on the length of the lease within the SIPP.

We have a wealth of information and case studies about putting commercial property in a SIPP on our website.

What these comparisons mean for you and your clients

The purpose of illustrating these comparative methods of charging is not to compare IPM’s charges with those of other providers.

We accept that these tables look favourable to IPM! While this was not our aim when we set out on this exercise, it does reinforce our belief in the benefit of charging on a predominantly fixed-fee basis, which is the way we have always operated.

This way, clients always know in advance what their fee to IPM is going to be, year in, year out. It also makes it easier for advisers and planners to explain to their clients how much an IPM SIPP will cost.

See how our SIPP offers complete investment flexibility for a fixed fee.

Get in touch

If you’d like to explore how our fee structure can offer value to clients, please get in touch. Email info@ipm-pensions.co.uk or call 01438 747151.