SIPP contribution refresher: Annual Allowance, carry forward, and the MPAA

This article is intended for financial services professionals only. None of the information contained in this article should be received as advice. Pensions are a complicated area of financial planning and IPM suggests that financial advice from a suitably regulated financial adviser is sought before an individual takes any action in respect of their pension savings.

We are confident that any advisers or team members at a regulated financial planning business will be familiar with the basics of making contributions to a SIPP:

- Contributions can be paid to a SIPP by the SIPP beneficiary, their employer, or a third party.

- Tax relief is available on contributions, but how this applies and how much can be received can vary based on an individual’s circumstances.

- Where the SIPP beneficiary or a third party contributes, IPM will reclaim 20% of this amount as tax relief from HMRC and apply this to the SIPP. If the beneficiary is a higher or additional rate taxpayer, additional tax relief may be due personally.

- Employer contributions are paid gross, i.e., IPM would not reclaim tax relief as described above. However, the contribution could qualify for corporation tax relief for the company making the payment.

While these principles sound simple, as with most things pension related there are nuances in HMRC guidelines which can impact the advice advisers may give.

With this in mind, we thought a recap of the position in respect of making contributions to a SIPP would be useful.

Annual Allowance

While in theory there is no maximum limit as to what can be contributed to a SIPP, the amount of tax relief available is capped. Part of the measures in place to cap this is the Annual Allowance.

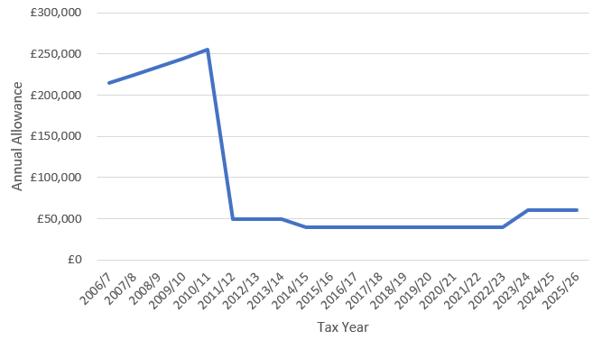

The term Annual Allowance was introduced as part of widespread changes in pension legislation in April 2006, or pension simplification as it became known (remember that!?)

From April 2006, an individual could contribute up to the lower of the Annual Allowance or 100% of their earnings and receive full tax relief. For employer pension contributions, there was no test against earnings.

For 2006/07, this was set at £215,000 and then increased by £10,000 a year until 2010/11, when the Annual Allowance was set at £255,000.

The government realised that this was probably a bit too generous. So, in 2011/12, we saw a drop in the Annual Allowance to £50,000. Since then, it has hovered around this level, bringing us to the current Annual Allowance of £60,000 for 2026/27.

It is important to remember that the Annual Allowance applies to contributions to all pensions an individual is a beneficiary of, including any benefit accrual in defined benefit (DB) arrangements.

Contributions made by an individual or a third party that is not an employer on their behalf cannot exceed the Annual Allowance or their earnings for that tax year. The tax relief would be limited to the lower figure; the actual contribution an individual can make and receive tax relief for would be limited to whatever their earnings are if these are lower than the Annual Allowance.

Employer contributions are not limited to an individual’s earnings, but the Annual Allowance still needs to be taken into consideration. Whether an employer contribution qualifies for corporation tax relief would be a question for the company’s accountant.

Carry forward of unused Annual Allowance

It is also possible to carry forward any unused Annual Allowance. This can be done for up to the previous three tax years, in theory allowing people to make a contribution of £240,000 in 2026/27 (£60,000 Annual Allowances for each of the 2023/24, 2024/25, 2025/26, and the current year) and receive full tax relief.

There are, however, some caveats with this:

- The individual must have been a member of any registered pension scheme for the tax years from which they wish to carry forward from, even if they are a deferred member of an old employer’s scheme. It would not be possible to set up a SIPP today and then use carry forward for an individual who had not previously been a member of any other pension scheme.

- Any contributions from previous tax years must be taken into consideration; this would include accrual in DB schemes. If a client had made a £20,000 contribution in the previous tax year, for example, only the unused £40,000 could be carried forward.

- Like we saw above, just because the Annual Allowance is set at a certain level doesn’t necessarily mean that tax relief at this amount will be available. Any personal or third-party contributions are eligible for tax relief at the lower figure of the Annual Allowance or the individual’s earnings in the tax year the contribution is being paid, i.e., it is not possible to carry forward earnings as is done with the Annual Allowance.

- The position is the same as set out as above for employer contributions.

Tapered Annual Allowance (TAA)

The TAA can see the Annual Allowance reduced from the standard level for high earners, down to £10,000 in some instances.

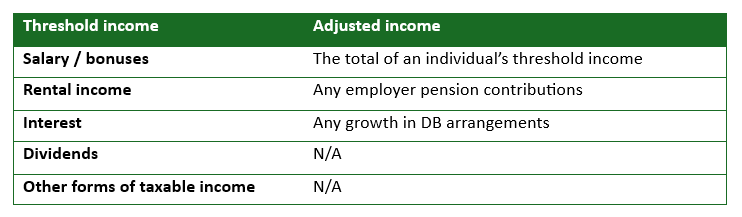

The TAA will kick in when an individual has a threshold income of £200,000 or more and an adjusted income of more than £260,000.

Put simply, for every £2 over £260,000 adjusted income an individual has, the Annual Allowance reduces by £1. The lowest TAA threshold of £10,000 is reached when an individual’s adjusted income reaches £360,000.

If you have clients with incomes in and around these figures, it is important to take time to calculate their threshold and adjusted incomes to ensure they are not impacted by the TAA. The following is not exhaustive; however, it shows what is usually included for calculating threshold and adjusted incomes:

As seen, employer pension contributions count towards adjusted income. Therefore, if you’ve got clients who are paying large sums from their company into their SIPP, care will need to be taken to ensure that this does not trigger the TAA.

Money Purchase Annual Allowance (MPAA)

The MPAA is another scenario whereby the Annual Allowance can be reduced from the standard amount. However, rather than having to carry out calculations like with the TAA to ascertain whether the MPAA will apply, the MPAA is triggered when certain actions are taken in a SIPP:

- Taking income from any flexi-access drawdown arrangement.

OR

- Taking an Uncrystallised Funds Lump Sum Payment (UFPLS), as this includes drawing income flexibly.

Where one of the above actions takes place, the MPAA of £10,000 will apply across all pension schemes in that individual’s name.

As important as it is to know what can trigger the MPAA, it is also important to know what actions do not trigger it:

- Taking a pension commencement lump sum (PCLS) only and not drawing any income under flexi-access drawdown.

- Purchasing an annuity where the benefits cannot be flexibly accessed.

- Drawing benefits from most DB schemes.

Common mistakes we see when dealing with contributions

Pensions are renowned for being complex, and while an Annual Allowance of £60,000 will be sufficient for most individuals’ requirements, at the high net worth end of the market it is more likely that the above complexities will need to be taken into consideration.

In addition to these, there are several contribution-related scenarios we see that are worth considering before a payment is made.

Can a contribution be refunded? – There are certain criteria that need to be met for a contribution to be refunded once it has been made to a SIPP.

In general, employer contributions are non-refundable unless a genuine administrative error, as defined by HMRC, has been made.

For personal or third-party contributions, a refund of excess contributions lump sum can be made when the total contributions made in a tax year exceed the maximum amount that an individual can receive tax relief for. For example, if an individual has made a personal contribution of £60,000 but their earnings for that tax year ended up being £50,000, a refund of £10,000 may be possible under some circumstances.

Rental income being seen as contributions – this is something which can be confused, especially if the client’s company is a tenant of a property that is owned by the SIPP.

Rental income is viewed as investment yield and does not count towards the Annual Allowance. In the scenario that the client’s company occupies the property owned by the SIPP, the company must pay the rent to the SIPP as per the terms of the lease and would then be able to make contributions to the SIPP in addition to this.

Paperwork, paperwork, paperwork – we know that filling out forms is not high on everyone’s list of fun things to do, but where someone is making a contribution to a SIPP, they must declare this intention before the payment is made.

For IPM, this can either be done on our application form when setting up the SIPP or by filling out our additional contribution form with the amount due to be paid and who is paying it (i.e., the individual or the employer) clearly stated. For anti-money laundering purposes (AML), where contributions are made by electronic transfer, IPM must also receive evidence of where the funds have been paid from. For regular contributions of the same amount, these paperwork requirements only need to be carried out once.

Get in touch to discover how IPM can support you and your clients

Our team are here to provide expert support on complex SIPP cases. Email info@ipm-pensions.co.uk or call 01438 747151.