A recent change to SIPP charging you might have missed

At the end of last month, the FCA released a raft of documents relating to pensions.

The paper that generated the most headlines and column inches was the proposed contingent charging ban on Defined Benefits (DB) transfers to Defined Contribution (DC) arrangements. DB transfers have rightly attracted a lot of attention in the last couple of years, and many of the advisers we work with have told us that the measures proposed by the FCA are something which they do anyway.

While all the focus was on DB transfers, you may have missed another FCA report that flew under the radar. Called Effective competition in non-workplace pensions, it tackled the concern that consumers are not always aware of the charges they are paying for their pensions due to the complexity of the fees.

Here, we break down the main findings of the report and what it means for you and your clients.

What the FCA says about non-workplace pension charging

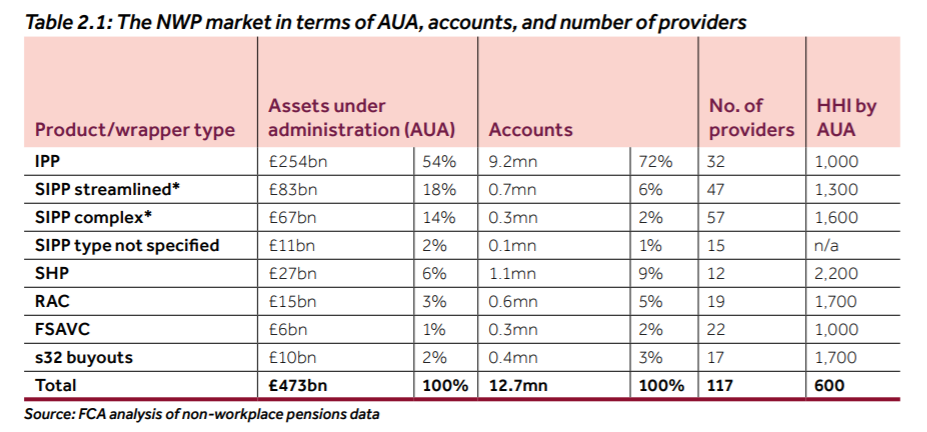

The market for non-workplace pensions is large. There are 12.7 million non-workplace pensions accounts, more than 100 providers or operators (life companies, investment managers, platforms and specialist operators) and around £470 billion assets held or invested (Assets Under Administration, or AUA).

In recent years, the FCA has become concerned that consumer engagement with non-workplace pensions, such as SIPPs, has been too weak. They say: “In the non-workplace pensions market, complex products and charges mean consumers cannot make comparisons easily and so are reluctant to switch.”

To combat this issue, the FCA is proposing that firms provide much clearer information about the total charges that a client will incur, and the impact of these charges at the point of sale and on an ongoing basis.

The FCA says the aim of this remedy “would be to raise awareness of charges and their impact on the value of consumers’ pensions savings and to increase the potential for consumers to make more informed decisions.”

The FCA wants providers to regularly present all charges in different categories in a standardised format (including ‘pounds and pence’ charges) so consumers can compare products.

They also believe it will incentivise a provider to explain how their charges compare given the features of their products and services. This may be done by reporting the charges to the FCA who would then collate and publish the information.

There are four main types of charge that consumers pay for their non-workplace pension:

- Mandatory product charges – these are charged by the pension provider for providing a non-workplace pension and include mainly administration charges that all consumers generally pay. Most of these are ongoing charges, while some can be a one-off (e.g. a set-up fee)

- Contingent product charges – these are also charged by the pension provider but are only paid by consumers that take certain actions, such as dealing in shares or exit fees for surrendering the policy before the end of the term

- Fund charges – these are charged by the fund manager for running the funds the pension is invested in. These charges include the ongoing charge figure (OCF) and other additional charges, such as fund transaction charges and fund performance charges

- Advice charges – these are charged separately by regulated advisers. Before RDR, providers paid commission to advisers and recovered that cost from the consumer through product charges.

So, that’s the background to the FCA’s changes. Next, we look at what it means for you and your clients.

Helping you to compare the cost of pension providers

Overall, we welcome the idea that there will be a central source which displays the wide range of charges levied by SIPP operators.

Advisers often ask us to help them when they want to compare IPM’s charges with our competitors. And, despite dealing with SIPPs every day, sometimes we struggle to make sense of some of the charging structures that are used!

Charges can vary based on a range of issues, such as the percentage of fund value and the number of investments made. While we appreciate the importance of each provider needing to make a profit, it does makes it difficult for advisers and clients to ascertain what fees they are going to be paying to their SIPP provider on an annual basis. In addition, some providers’ charging structures are very complex.

Read more about IPM’s fixed and competitive fee structure

IPM’s charging structure lends itself well to any regular reporting required. Our flat annual administration fee (which has remained at the same level since 2001), the fact we charge no establishment fee, fee for transfers in, or fee for contributions or making investments (other than commercial property) makes it easy for us to outline what our charges are.

IPM also levies a flat annual drawdown fee with no additional charges for taking income or varying the levels being paid.

Reporting fees and charges could be more difficult than the FCA believes

From a transparency point of view, this report is a welcome development.

However, the FCA’s paper differentiates between streamlined and complex SIPPs and we believe it would be good for this be reflected in the charges comparison. Comparing a restricted, online SIPP offering against a full SIPP which offers a wide range of investments and ways to draw benefits is not comparing like-for-like products.

For bespoke providers, such as IPM, providing details on fund charges in a regular report format will not be straightforward. For example, we do not operate a panel of funds or investment houses that clients must select from.

In addition, when considering commercial property purchases, a tariff of charges will need to include all third-party fees such as those from solicitors, surveyors, banks and so on. The question remains: how are these charges supposed to be reported?

What the future could look like

Overall, we generally welcome the FCA’s idea of cost disclosure and understand what they are trying to achieve. If presented correctly, a comparison of charges can help clients to understand exactly what they paying in return for the services they are provided with. We’re all for clarity and people being able to access information easily!

However, for complex SIPPs, we’re unsure how all associated charges not levied by the SIPP provider can be reported in a pre-agreed format on a regular basis. A ‘one size fits all’ approach to this kind of work does not really work for complex SIPPs.

Reporting could potentially work on an individual, ‘per client’ basis but this would involve changes in processes and systems for complex SIPP operators.

Perhaps a starting point could be for SIPP providers’ charges to be separated between streamlined and complex SIPPs when presented. This could encourage the consumer switches the FCA seems keen to encourage in the right circumstances.

Then, other specific costs could be looked at separately, rather than bundling everything together. Perhaps on a scenario-based approach: for example, a client with £500,000, two ‘transfers in’, investing on XYZ platform charging 0.5% per annum with ongoing fund charges of 0.7%.

If you have any questions about our fees, or the wider issue of charging structures for SIPPs, please get in touch. Email info@ipm-pensions.co.uk or call 01438 747 151.