5 client scenarios where a bespoke SIPP can help

This article is intended for financial services professionals only. None of the information contained in this article should be received as advice. Pensions are a complicated area of financial planning and IPM suggests that financial advice from a suitably regulated financial adviser is sought before an individual takes any action in respect of their pension savings.

We have previously looked at the various types of SIPPs that are available in the market.

We understand that a lot of our advisers will have a default, low-cost simple SIPP that satisfies the requirements of most of their clients. It’s when this type of platform SIPP cannot accommodate your client’s requirements that we want IPM to be your first choice.

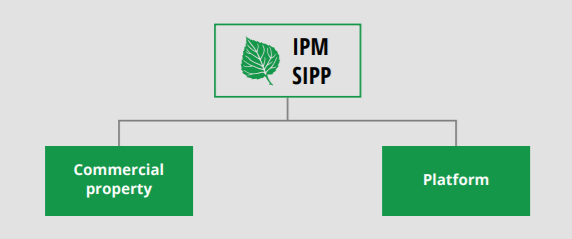

IPM are experts in commercial property purchase within SIPPs. It is a reputation we are proud of:

- We own over 1,200 properties within our Scheme on behalf of clients.

- Typically, we have around 100 property transactions ‘on the go’ at any one time.

- IPM employs a specialist property team, a member from which is allocated to each individual transaction giving you and your client a named point of contact from instruction through to completion and beyond.

- Our charging structure for SIPP property purchase is amongst the most competitive in the market, as we do not charge an annual property fee in addition to our annual administration fee.

While this is a reputation we are proud to hold, there are a variety of other SIPP-related scenarios that IPM can help your clients with.

Here are five times IPM should be the first choice SIPP provider for your client.

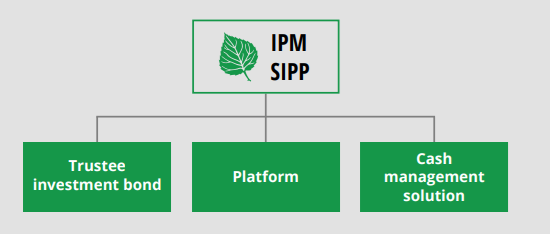

1. Multiple investments in a SIPP

As mentioned, for a lot of your clients a simple, platform SIPP will cater for all their investment needs, regardless of the size of fund value.

However, where your client requests a specific investment strategy that cannot be accommodated on a platform, or perhaps as an adviser you recommend investments over several different institutions, you are going to need a SIPP provider that can facilitate this.

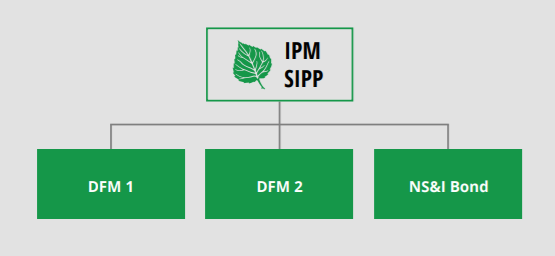

IPM does not operate panels of investment houses that your clients must select from. You can select any platform, discretionary fund manager, bank, cash management solution, bond provider, or stockbroker that meets your clients’ requirements, subject to IPM’s internal assessments being undertaken.

- You may have a client who wants to select some investments themselves, so alongside a platform, you can open an execution-only stockbroker account.

- Have a client that is risk-averse? You can open accounts with banks that accept third-party deposit accounts or cash management solutions such as Insignis to sit alongside your usual investment house. We can also hold some NS&I products, to give clients a higher level of financial protection.

- PruFunds continue to be a popular investment choice for our advisers. To access these via a SIPP you need to open a trustee investment bond with Prudential. We can do this and hold the bond within the IPM SIPP together with any other investment recommendations you make.

These are just a few examples, but there are many different possibilities IPM can accommodate.

We also do not make any additional charges when you open multiple investment accounts within a client’s SIPP. Nor do we charge transaction fees to move monies between the various firms and the trustee bank account.

This gives you full flexibility in tailoring a SIPP specific to your client’s requirements, together with the confidence you can do this without incurring significant fees from your SIPP provider.

2. Clients who live outside the UK

For many people, a long-held dream when they retire is to escape the British weather and move to a country with a warmer climate.

Also, it is not unusual for people to come to the UK for a period to work before returning home.

In addition to the above, technological advances now allow people to work anywhere in the world in certain industries or professions.

All these scenarios can have one thing in common: people abroad who may have accrued UK pension benefits.

Pension providers take different approaches to clients who do not reside in the UK. In some instances, providers will not continue to provide a service to clients who do not live in the UK.

IPM does not take that blanket approach and will assess each scenario on a case-by-case basis. However:

- Where a new SIPP is being established, IPM will only do so where advice is being given by a financial adviser regulated by the Financial Conduct Authority (FCA).

- In this scenario, we will only accept transfers from other UK-registered pension schemes as a way of funding the SIPP.

- IPM are not overseas tax experts. How a UK SIPP is treated in the country in which the client resides is a matter for an individual to deal with personally.

There are instances in which we can run a SIPP in currencies other than GBP. This can be particularly beneficial when someone is looking to draw benefits from the SIPP.

You may find our article about how we work with overseas clients to be helpful.

3. Clients who wish to invest in non-standard assets

Let’s be clear, when we talk about non-standard investments we are not thinking about some of the high-profile investments that have lost people significant amounts of their retirement pots and seen SIPP providers fall into the Financial Services Compensation Scheme.

Nor are we looking to purchase works of art, classic cars, or other tangible, moveable assets within our Scheme.

Over a decade ago, the FCA split SIPP investments into ‘standard’ and ‘non-standard’ to help prevent some of the poor outcomes clients had faced in the SIPP space. While broad, in general terms, a non-standard asset is one that cannot be traded within 30 days, is illiquid, or is not regulated by the FCA.

Examples include:

- A bond held offshore

- A quarterly dealing hedge fund for an experienced investor

- A previously liquid, daily trading fund (such as a property fund) where withdrawals have been suspended

- Some cash products, as these cannot be broken within 30 days!

We are not looking to attract a high volume of these types of enquiries. But we appreciate that from time to time a client’s circumstance may call for a more bespoke approach, which will include a non-standard investment. We are always happy to have a conversation with advisers about whether IPM is able to help.

4. Transfers in-specie from other SIPP / SSAS providers

On occasion you may have a client who has a SIPP elsewhere that cannot accommodate what they are looking to do or is unhappy for some reason (could be service, could be costs, could be both). Or, you have clients in a SSAS that, while originally serving their requirements, no longer need the complexity of that type of arrangement.

If that client is looking to switch provider, it may be that the transfer is to be made by way of assets instead of cash, i.e., a transfer in-specie.

Transfers in-specie from other SIPPs and SSASs are something IPM undertake on a regular basis. While not as straightforward as simple cash transfers, with a bit of pre-planning before a recommendation is given to a client, IPM can assist you in the steps needed to ensure as smooth a transition as possible.

- Do we need to set up a platform / DFM account to receive any assets currently held with the current provider?

- Certain types of bonds may require a deed of assignment; we can help with that.

- Other assets may require specific forms to be completed by the investment house to facilitate a transfer.

- If the current arrangement holds a commercial property, this is a different ball game. Thankfully, this is also an area IPM is hugely experienced in and can help.

Or it could be a case we talk through with an adviser why a certain transfer may not be possible.

As we considered earlier, given IPM’s flexibility regarding the investments that can be held in our SIPP together with our cost-effective fee structure for SIPPs with multiple investments, which often includes no additional fees for transfers in-specie, this is an area we can help with.

5. Old-fashioned customer service

The technological advances over the past couple of decades have transformed financial services, like most industries.

You can now open an ISA online in ten minutes, make investments at a few clicks of a button and who knows where we will all be in five years’ time with AI!

While this is all great and IPM embraces these technological advances where we can, some people still value being able to pick up the phone and speak to someone, having a point of contact, calling in a favour when needs be, or just having some support on a particularly difficult scenario. This is where IPM stands out amongst our competitors.

IPM was built around providing high levels of service to our clients and introducers. We have never wanted to be the biggest SIPP provider; we simply wanted to be the best we can be.

We accept that there will be other SIPP providers out there with greater online capabilities and will be able to service your clients’ needs. And that is fine.

However, there will always be those clients that require more of an attentive service, whether their needs are truly bespoke or they require a more personalised service.

In an ever-changing world we will still be here providing that continuity of service, security, and reliability in the SIPP world that we have been doing for over 25 years.

Get in touch

To discuss anything you have read about here, or to learn more about our offering, please contact us. Email info@ipm-pensions.co.uk or call 01438 747151.